Debt Relief May Trigger Tax

The Mortgage Debt Forgiveness Act, originally passed in 2007, was extended three times to protect homeowners from paying income tax on debt that was relieved due to foreclosure, short sales or deed in lieu of foreclosure.

The law expired on December 31, 2016 and unless it is extended again, homeowners with debt relief in 2017 may be subject to tax.

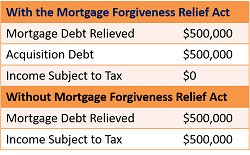

A homeowner might feel a sense of relief without the obligation of a delinquent mortgage but just because the payments are no longer due doesn’t mean that there isn’t another obligation that replaces it. If a lender cancels or forgives debt, a taxpayer must include the cancelled amount in their income for tax purposes depending on the circumstances. The tax significance could be serious.

This previously allowed relief only applied to a taxpayers’ acquisition indebtedness of their principal residence which did not include second homes and investment property. The maximum amount was limited to $2 million of mortgage debt forgiveness or $1 million if filing separately.

Due to the serious consequences involved in short sales and foreclosures, it is advised that homeowners faced with this possibility should seek expert advice from their legal and tax professionals.

The law expired on December 31, 2016 and unless it is extended again, homeowners with debt relief in 2017 may be subject to tax.

A homeowner might feel a sense of relief without the obligation of a delinquent mortgage but just because the payments are no longer due doesn’t mean that there isn’t another obligation that replaces it. If a lender cancels or forgives debt, a taxpayer must include the cancelled amount in their income for tax purposes depending on the circumstances. The tax significance could be serious.

This previously allowed relief only applied to a taxpayers’ acquisition indebtedness of their principal residence which did not include second homes and investment property. The maximum amount was limited to $2 million of mortgage debt forgiveness or $1 million if filing separately.

Due to the serious consequences involved in short sales and foreclosures, it is advised that homeowners faced with this possibility should seek expert advice from their legal and tax professionals.

DON BURNS TEAM- REAL ESTATE

as one of the TOP 500 Top Producing

Teams/Individuals in Texas

CDPE, CRS, ePRO®

http://www.har.com/donburns

don@donburns.com

(281) 491-6274

(281) 734-8715

Comments

Post a Comment